The Ergodic Forgot-it

Published on

Contents

I found a nice lunch-break series on youtube from some economics nerds here on ergodicity in economics . It is worth a few comments.

These are econophysics bros, but among the finance bro nerds, these guys seem to be of the decent variety. There is a trace of a hint of some level of concern for the plight of the poor in their work.

Wealth Reallocation Models

There are many simple models for how financial wealth gets distributed. Unfortunately most are politically neutral or politically agnostic. So all are unrealistic. However, they are empirically accurate. How can that be?

Firstly, modelling macroeconomics is a lot like some aspects of statistical mechanics, where there can be phenomena akin to multiple realization: meaning more than one underlying dynamics or set of governing rules could determine the same qualitative macroscopic behaviour.

Secondly, in the real world governments do not behave as if they have a monopoly control of their own tax credits (aka. the currency) and so a lot of economic injustices occur due to plain ignorance — massively tragic form of banal evil. If governments cause unemployment in the first place (as MMT shows) then a morally agnostic government operating according to quasi free market ideology — welfare for the rich, rugged individualism for the poor — will practically guarantee end results that are Pareto tailed — the rich get richer.

The econophysics bros models capture such politically “agnostic” dynamics. Only the problem is they fail to realize this is political mismanagement on an epic and tragic scale. It is not agnosticism at all.

Sure, you might be justified in claiming absent a currency monopoly there would be some kind of free market, then those models become applicable. The result is a free market always evolves to extreme injustice — highly unequal distribution of financial wealth. (Hence real wealth too, since financial wealth equates to real purchasing power. The more money (scorepoints) you can rake in from rentier activity, the more you can purchase without reduction in your hoard of financial scorepoints.

I am not claiming any particular reason the econophysics models seem to accurately account for real world wealth distribution, just pointing out some possible explanations. Butone thing is for certain: the real world data is drawn from nations that run MMT systems. So it is clear that governments in these nations have the operational ability to eliminate the Pareto tails and ensure fair & just wealth distributions. Meaning if politics were good, serving the public purpose, then the econophysics bro’s ‘models would be wrong.

That is really my main point today.

The econophysics models might be correctly capturing some aspects of macroeconomic real-world dynamics, but the main point to make is that this does not mean the real world should be as it is: we could do much better.

Negative $\tau$

The simple stochastic geometric Brownian motion model for wealth reallocation is definitely a politically agnostic model, so pretty disgusting. But that is because our political economy is pretty disgusting. Yes, for sure, all you Enlightenment nerds: human civilization has progressed for the good, in so many ways, but that does not imply we are at a stage of decent political economy. It just means all past human history where power elites have been found, it has been diabolically nasty and brutal.

In Yonatan Berman’s model the main control parameter $\tau$ allows for interactions between individuals, and this is what allows the dynamics to become non-ergodic.

It is seriously important in the econophysics, because ergodicity is thought to be characteristic of the real-world under typical circumstances. The long time average of a distribution of wealth is the same as the average over all infinite possible ensembles.

((Why so seriously important? It is because these econophysics models are all about the statistical mechanics, so the statistical characteristics are the only thing they need to get right, so they need to get (non)ergodicity — and other statistical characterizations — right, if nothing else.))

Models where the time average does not equal the ensemble average are non-ergodic, and this is the real-world situation when there are increasing returns to wealth and decreasing returns to the poor. The Gilded Age, the Great Depression, and the Neoliberal era, are possible non-ergodic periods in our recent history, times when the rich got not only richer, but obscenely richer — in relative terms.

The base model is random multiplicative growth — which means the growth in wealth over a distribution is dominated completely by random exchange. This is non-ergodic.

The first adjustment for reality is a reallocation term, with parameter $\tau$, which governs how one individual contribute aa fraction of their wealth every time period to a common pool, this pool is then split evenly between everyone. The model is very simple, $$ dx_i = x_i \left(\mu \, dt + \sigma\, dW_i (t)\right) - \tau\left(x_i - \braket{x}_N\right)\, dt $$ The first term in parentheses is the geometric Brownian random exchange effect, the second is the reallocation.

For simple analysis $\tau$ is taken to be the same for everyone, which means the amount of wealth put into the common pool is the same proportion of an individual’s current wealth. The rich contribute more than the poor, but in equal percentages.

For $\tau>0$ people with wealth greater than the population mean $\braket{x}_N$ is a net contributor, while the poorer are net receivers. This is the ergodic regime.

(Technically, the reallocation model is ergodic if $\tau > tau_c$ for some threshold $\tau_c$, but for a large enough population $\tau_c \approx 0$.)

In the ergodic regime rescaled wealth converges in time. Although it still has a “disgusting” Pareto tail (technically an inverse $\Gamma$ distribution), it is at least telling us that government have a role to play in fairly redistributing nominal wealth. Why? Because in the real world everyone knows redistribution does not occur. The rich can afford tax evasion, and the poor not only have a tax burden but also tend to need to borrow from banks just to not starve — through no fault of their own (why the hell are they being taxed? There is no good reason.)

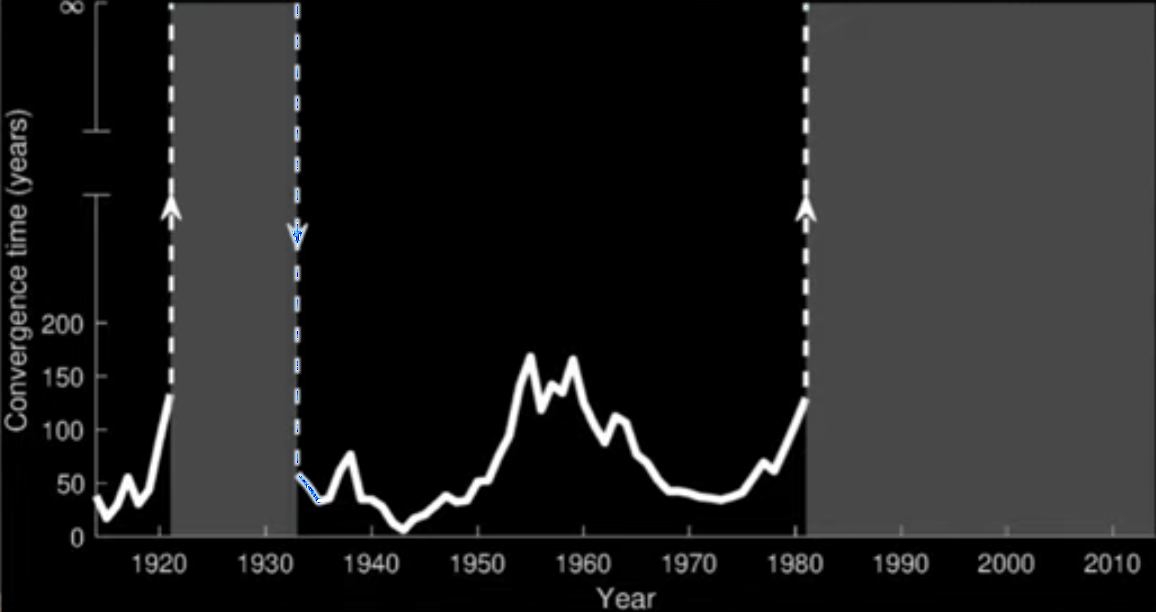

In particular, the models show that in times when in the real world the effective $\tau <0$ are times of increasing return to the rich, when inequality soars. These are non-ergodic periods. It is pretty revealing to see the data estimates showing the periods in recent history where such instability occurs, the following screenshot is Barman’s data.

The light grey bands are the regions where $\tau <0$ for the USA, the non-ergodic regimes where wealth inequality grows and people with negative wealth arise.

For $\tau < 0$ the dynamics are non-ergodic. One interesting thing is that Berman characterizes this regime by the effect on the poorest:

In this regime some individuals end up with negative wealth, even if all start with positive wealth.

The long neoliberal era period from 1980 to today where $\tau < 0$ is as story of a new gilded age. Crushing for the poor and the working middle class. Boom times for the rentiers and grifters.

Currently then, under present government policy, pretty much across the world, we are in a terrible era of non-ergodic wealth allocation effects, $\tau < )$, and the reallocations are from the poor to the rich.

What it also shows is that the default assumptions in mainstream economics: that reallocation is ergodic, are unjustified, and often downright invalid. But that is the most mild criticism of mainstream economics. I mean… hells bells… everyone knows the political economy is unjust, we did not need a model to tells us this is due to non-ergodicity. Without incredible unheard of charity and altruism on a global scale, it’d be unjust even in the ergodic regimes, given present neoliberal policy dominance.

What more can be said?

Well I know: a helluva lot more. People need to know MMT. Governments need to know what the full policy space available to a monopoly currency issuer is, if only so they know their policy is designed to benefit the rich and crush the poor. The first step to denouncing neoliberalism is to know what the policy does and why the policy is stupid, at best, horrific class warfare at worst, tantamount to murder by government design or ignorance.

You cannot claim moral righteousness if you think there is no alternative.

Interest Rate Effects

Although MMT scholarship is pretty clear in interest rate effects, it is not crystal clear, because the macroeconomics is highly non-linear and dynamical and non-linear. Interest rate have “perverse” effects, meaning they can be pro-inflationary (most oftne) but under some conditions can stifle effective demand.

The LSE EgodicityEcon group have a write-up where they advocate low interest rates, but I thought they offer an incorrect analysis, so I wrote this comment to them:

Hey, in your write-up https://ergodicityeconomics.com/2017/08/14/wealth-redistribution-and-interest-rates/ you get interest rates slightly wrong. Most loans are fixed rate, so lowering the interest rate does not help the poor too much, except to slow down inflation. High rates are one-to-one pro-inflationary through interest-income and forward price effects, given propensities of savers to spend and borrowers to save are empirically about equal. But in fact moderate inflation helps with a bit with fixed rate debt, since it means higher nominal income servicing a fixed rate debt. It still sucks that most lower income families in debt have to also pay higher CPI prices, but nevertheless, if they stay afloat a moderate rate of inflation helps them pay off fixed rate debts faster. Which means a higher interest rate tomorrow helps them to pay off past lower fixed rate debt.

The more serious inequality issue is with debts that cannot be repaid out of income flow.

Debts that cannot be paid should be forgiven, since in the macro they are a drag on effective demand or currency circulation, and we all know healthy effective demand is a healthy economy. Debts that can be repaid can be serviced out of income flow. That suggests decent wages buttressed by a Job Guarantee wage floor is the superior policy to ineffective monetary policy. It is called fiscal dominance.

Yeah, central bank interest rates should be permanent zero (ZIRP) and this is non-inflationary, once you understand the source of the price level. Chartered banks can always operate for a profit from the spread rate, and they always do, they can make loans regardless of the CB rate. The constraint on bank credit is the number of credit-worthy borrowers. Banks do not lend reserves or deposits, they issue credit simply by marking-up the customer’s bank account, the currency is created ex nihilo, in receipt of a promissory note to repay (also in the form of a credit card agreement). The licensed software operationally does not permit a bank to lends reserves or deposits. Moving around deposits is what non-bank trusts need to do, since they do not have access to the legal means to create the currency ex nihilo, if they tried they’d be jailed for counterfeit. Chartered banks do not operate like this, they have a license to create the currency ex nihilo by computer account entries (albeit with severe penalties for fraudulent issuance — they do need to find or “generate” a credit-worthy borrower).

Guess what helps create more credit-worthy customers? — a higher CB rate, since the CB/Treasury rate is essentially a basic income scheme: basic income but only for people who already have money in proportion to how much money they already have.".

Follow-up:

As for folks who fear forgiving debts can lead to instability and rampant inflation, let me just say they are ignoramuses. Effective demand has never been a cause of hyperinflation (the causation goes the other way, with usually war reparations, massive corruption, or severe natural disasters the cause), and moderate inflation is a good thing — it erodes the purchasing power of hoarded wealth, encourages more circulation and reduces the burden of past debt, provided wages go with. The way to get wages “going with” is via Job Guarantee wage floor. The CB sets the interest rate floor by votes, the Parliament must set the wage floor, also by a vote. There is no market force obstacle at play for a monopoly currency issuer, unless the politicians falsely act as if there is market pressure. They can tell the bond traders to pi55 off. The government does not need to borrow it’s own fiat currency.

Tax returns and bonds do not finance the government. Taxes help resource the government in real terms — the tax liability generates demand for the otherwise worthless currency. Tsy Bonds are an interest rate maintenance operation, an asset swap, not a borrowing operation.

And the discipline on banks has to be understood. It never works out if the liability side is chosen as the place for discipline. For starters no customers know the risk, to think they do is laughable. The proper place for discipline is on the asset side. The proper policy is to give banks unlimited overdraft at the CB, to ensure payments clearing, and discipline the banks on the asset side. You tell banks only what they can do, and that is to (1) run the payments clearing, (2) assess credit worthiness. Do not allow them anything else. Bankers are dangerous animals and need to be kept in cages.

Quite a bit of channelling Mosler the GOAT there, which I will always do given half a chance.

All We Need is a Warp Drive

I want to return to my main point:

The econophysics models might be correctly capturing some aspects of

macroeconomic real-world dynamics, but the main point to make is that this

does not mean the real world should be as it is: we could do much better.

And we can do better without any heavy-handed social engineering or forced communism or the like. We can do better simply if, (a) governments understand they have at least tow unique and powerful monopoly instruments (the legal and the monetary system, the former includes military and police power). And (b) we have real serious democratic control of our governments, meaning they bend to “the people’s” will, not to the will of the oligarchs.

When I write, “simply if” please know that I realize this does not mean politically or sociologically simple. It means operationally simple. The politics messes you up. “All we need is the correct moral and ethical political will to do good…”, is a phrase a lot like interstellar travel plans: “All we need is a Warp drive…”.

However, I am not a pessimist nor nihilist. We can find this macroeconomics “warp drive”. It is not a scifi fantasy. That is because the macroeconomics warp drive is not a physical thing, it does not have to be materially engineered. It is a spiritual reality, it is love for other people, compassion, trustworthiness, humility, compassion, justice, mercy, forgiveness, wisdom. That is our political economy warp drive.

It costs nothing material to get it. It costs suppression of ego and greed. Which is why it seems incredibly hard to get. No one can legislate better morality. Moral and ethical transformation has to be learned, nurtured, grown, and fostered with the metaphorical water of wisdom and kindness.

Power

This is something everyone who learns MMT eventually comes to appreciate. MMT is a necessary step in the battle, but it is only a first step. Yeah, it can be taken in parallel with other steps.

But once you realize a government has amazing monopoly powers, you realize the magnitude of the task ahead. Those wielding that power fail to acknowledge MMT, and hide their wilful or innocent ignorance behind veils of “let the markets do their magic” parables. Such market ideology is in fact anti-democratic. But it gets endlessly paraded as a manifestation of democracy and freedom.

The task for pursuit of greater justice is thus truly immense.

We are talking biblical in scale, lest it be not obvious!

| Previous chapter | Back to | Next post |

| Noeoelectric Cars | TOC | Newsworthy |